For owners approaching or past the $1M mark, growth can hide a looming issue: cash. You can show a profit and still struggle to make payroll. This playbook explains how to manage cash flow with simple routines, better pricing, cleaner data, and forward-looking forecasts—so you can operate with confidence and invest in growth.

Cash Flow vs. Profit: Why It Matters

Profit is revenue minus expenses on your income statement. Cash flow tracks where money actually moves in and out of your bank accounts. The difference matters because big cash uses—like buying inventory, equipment, or repaying debt—don’t hit your profit and loss the same way they hit your cash.

If your P&L shows profit but your bank balance hasn’t grown, the missing story is in your cash flow statement and balance sheet—owner draws, inventory purchases, asset buys, and loan activity.

Common Warning Signs You Have a Cash Flow Problem

- Overdrafts and late bill payments

- Relying on a line of credit to cover routine expenses

- Difficulty making payroll or paying vendors on time

- Low or no cash reserves for unexpected expenses

These are not just headaches—they’re signals that your business systems (pricing, collections, expense control, or forecasting) need attention. Running out of cash is a top reason young firms fail, even with demand and revenue.

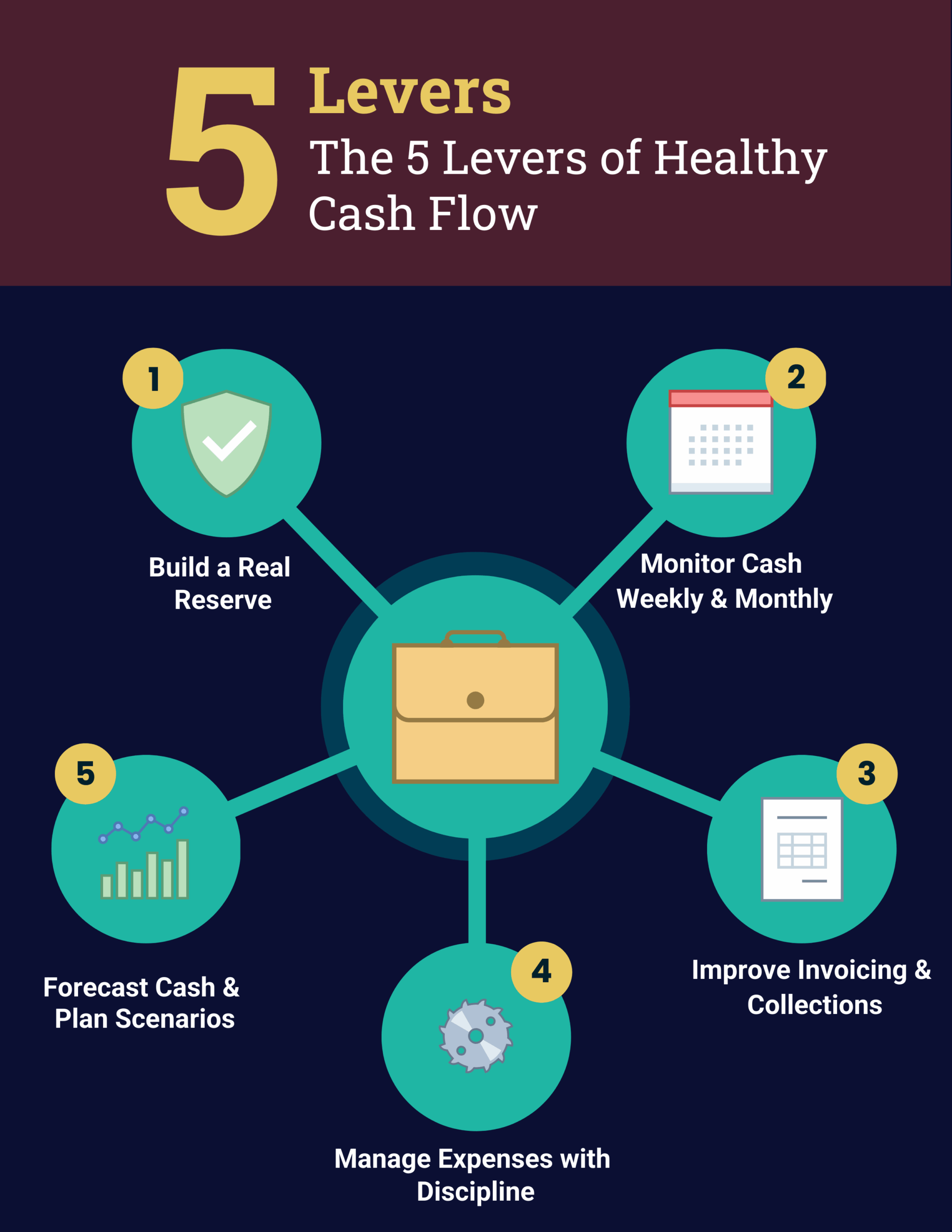

The 5 Levers of Healthy Cash Flow

1) Build a Real Reserve (3–6 Months of Expenses)

A cash reserve buys time and calm decision-making. Calculate an average month of expenses and multiply by 3–6.

Average Monthly Expenses = Total Expenses (Last 12 Months) ÷ 12

Target Reserve = Average Monthly Expenses × 3 to 6

Keep it liquid (high-yield business savings, short-term CDs you can access in <30 days). The peace of mind alone improves decision quality.

2) Monitor Cash Weekly and Monthly

Set short, repeatable meetings—even as a team of one.

| Cadence | What to Review | Decisions to Consider |

|---|---|---|

| Weekly (15–30 min) | Bank balances, bills due, AR aging, big expected inflows/outflows | Payment timing, collections calls, short-term holds |

| Monthly (45–60 min) | P&L, balance sheet, cash flow statement | Pricing tweaks, cost cuts, hiring plans, debt paydown |

| Quarterly (60–90 min) | Forecast vs. actual, KPIs, scenario plans | Capital investments, product/service mix, growth bets |

3) Improve Invoicing and Collections

- Invoice faster: send invoices on delivery or milestone completion, not “end of month.”

- Shorten terms: if you’re at Net 30, test Net 15 or progress billing.

- Make payment easy: accept ACH and card; add payment links to invoices.

- Follow a collections playbook: reminders at 3/7/14/30 days past due; escalate with a polite call and a late-fee policy.

- Assign ownership: someone must own AR and a weekly follow-up routine.

Also audit pricing annually. If inputs (labor, software, materials) rose but prices did not, margins and cash suffer. Fair, transparent increases protect service quality and stability.

4) Manage Expenses with Discipline

Run a vendor summary from your accounting system and ask, line by line: Do we need this? Are we double-paying? Can we negotiate?

- Cut unused or redundant software licenses (often 5–10% savings)

- Negotiate 1099 contractor rates or scope

- Shift processing fees when appropriate and transparent

- Review travel/meals for business relevance

Even trimming $2,000 per month frees $24,000 per year—enough to fund a key hire or accelerate debt reduction.

5) Forecast Cash and Plan Scenarios

A 12–18 month rolling cash forecast turns surprises into planned choices. Start simple in a spreadsheet, then graduate to forecasting tools as you grow.

- Baseline: revenue, collections timing, COGS, payroll, overhead, debt payments, taxes

- Scenarios: best case, base case, downside (e.g., 10–20% revenue dip)

- Decisions: hiring dates, capital purchases, price changes, loan draws

Good tools help you model “how long can we sustain a downturn?” and “what month do we cross a cash threshold for investment?”

Get Your Data Right: Cost Accounting and Accrual

To know which services or projects drive cash, you need more than basic bookkeeping.

- Accrual accounting: matches revenue and expenses to the period earned/incurred, giving a truer operating picture.

- Cost accounting: tracks labor, materials, and overhead by service or project to reveal true margins.

Garbage in, garbage out. Clean, consistent categorization and system integrations (payroll, invoicing, payments) are essential to trustworthy decisions.

Smart Use of Lines of Credit

Lines of credit are a cash flow tool, not a chronic lifeline. Use them to smooth timing gaps or fund short-term, high-confidence opportunities—paired with a clear payback plan. If you rely on debt to cover routine operating losses, fix the underlying operations (pricing, mix, costs, collections) first.

Tech Stack to Strengthen Cash Flow

- Accounting: QuickBooks Online, Xero, NetSuite

- Forecasting & reporting: Fathom, LivePlan, custom models

- Invoicing & payments: Stripe, Square, ACH via your bank; proposal-to-payment tools with built-in collections workflows

Integrate systems so AR, payroll, and expenses flow into one source of truth for timely reporting.

KPIs That Predict Cash Issues

- Operating cash flow trend (monthly)

- Days Sales Outstanding (DSO): how long it takes to collect

- Gross margin and contribution margin by service/project

- Cash conversion cycle (inventory + receivables − payables days)

- Months of cash on hand (reserve ÷ average monthly expenses)

Examples and Edge Cases

Delayed Payer Industries

If insurance or enterprise clients pay 60–120 days after service, your forecast must model the lag. Consider progress billing, retainers, or early-payment incentives to shorten DSO. In severe delays, assess low-cost, short-term financing or selective invoice factoring—with fees weighed against operational risk of missed payroll.

Owner Draws and Equipment Purchases

Owner distributions and asset purchases won’t hit your P&L as expenses, but they drain cash. Track them separately and build their timing into the cash forecast.

A 30/60/90-Day Cash Flow Plan

Days 1–30:

Stabilize

- Reconcile books; ensure bank/credit card feeds are current

- Build a simple 13-week cash forecast

- Run AR aging; send reminders; call top 10 overdue accounts

- Freeze nonessential spend; cancel redundant tools

- Set weekly cash huddle: balances, bills, AR, upcoming big items

Days 31–60:

Strengthen

- Implement progress billing or retainers

- Adjust payment terms; enable ACH/card on all invoices

- Negotiate vendor terms (Net 30–45) and discounts where possible

- Define pricing strategy; implement fair increases where inputs rose

- Document collections SOP with reminder cadence

Days 61–90:

Scale Confidently

- Stand up a 12–18 month forecast with best/base/downside cases

- Measure service/project margins (cost accounting)

- Set a target reserve (3–6 months) and automated sweep to savings

- Outline triggers for investment (e.g., maintain 4 months’ cash for 90 days)

- Review KPIs monthly; adjust plan based on actuals

How to Know It’s Working

- Bank balances trend up month over month (outside of planned investments)

- DSO declines as collections improve

- Stable or growing reserve balance

- Fewer cash emergencies; clear visibility into the next 13–26 weeks

- Decisions made from data, not stress

Trusted Frameworks and Further Reading

Cash discipline is a management habit. Regular reviews, clean data, and forward-looking forecasts turn growth into durable stability.

If you’re unsure where to start, begin with the 13-week forecast and a weekly cash huddle. Everything else becomes easier once visibility improves.

FAQ

How big should my cash reserve be?

For most small businesses, target 3–6 months of average operating expenses. Highly seasonal or slow-collecting industries may need more. Keep reserves liquid so funds are available within 30 days.

Why is my P&L profitable but my bank balance isn’t growing?

Profit excludes certain cash movements such as owner draws, inventory purchases, equipment buys, and debt principal payments. Review your cash flow statement and balance sheet to see where cash went, then adjust timing and policies accordingly.

How often should I review cash flow?

Run a brief weekly check for balances, bills due, and receivables, plus a deeper monthly review of the P&L, balance sheet, and cash flow statement. Compare actuals to forecast quarterly and update scenarios.

When should I raise prices?

Review pricing at least annually, or sooner if input costs rise, scope expands, or your service level has increased. Communicate changes clearly and tie them to value delivered to maintain trust and margins.

What’s the best way to start forecasting?

Begin with a simple 13-week spreadsheet forecasting inflows and outflows, then extend to 12–18 months. As complexity grows, consider tools like Fathom or LivePlan for scenarios and visual dashboards.

References

Next step

What’s the one cash flow hurdle you’re facing right now—collections, reserves, pricing, or forecasting? Comment below with your biggest challenge, and we’ll share practical next steps.