If you run a growing business, the fastest way to overpay the IRS is not a complex loophole—it’s poor recordkeeping. This guide explains the most expensive 2025 tax mistakes we see, how to fix them, and the simple workflow that keeps you compliant all year.

Who this is for: U.S. business owners, finance leads, and independent professionals who want accurate books, fewer surprises, and clean audits.

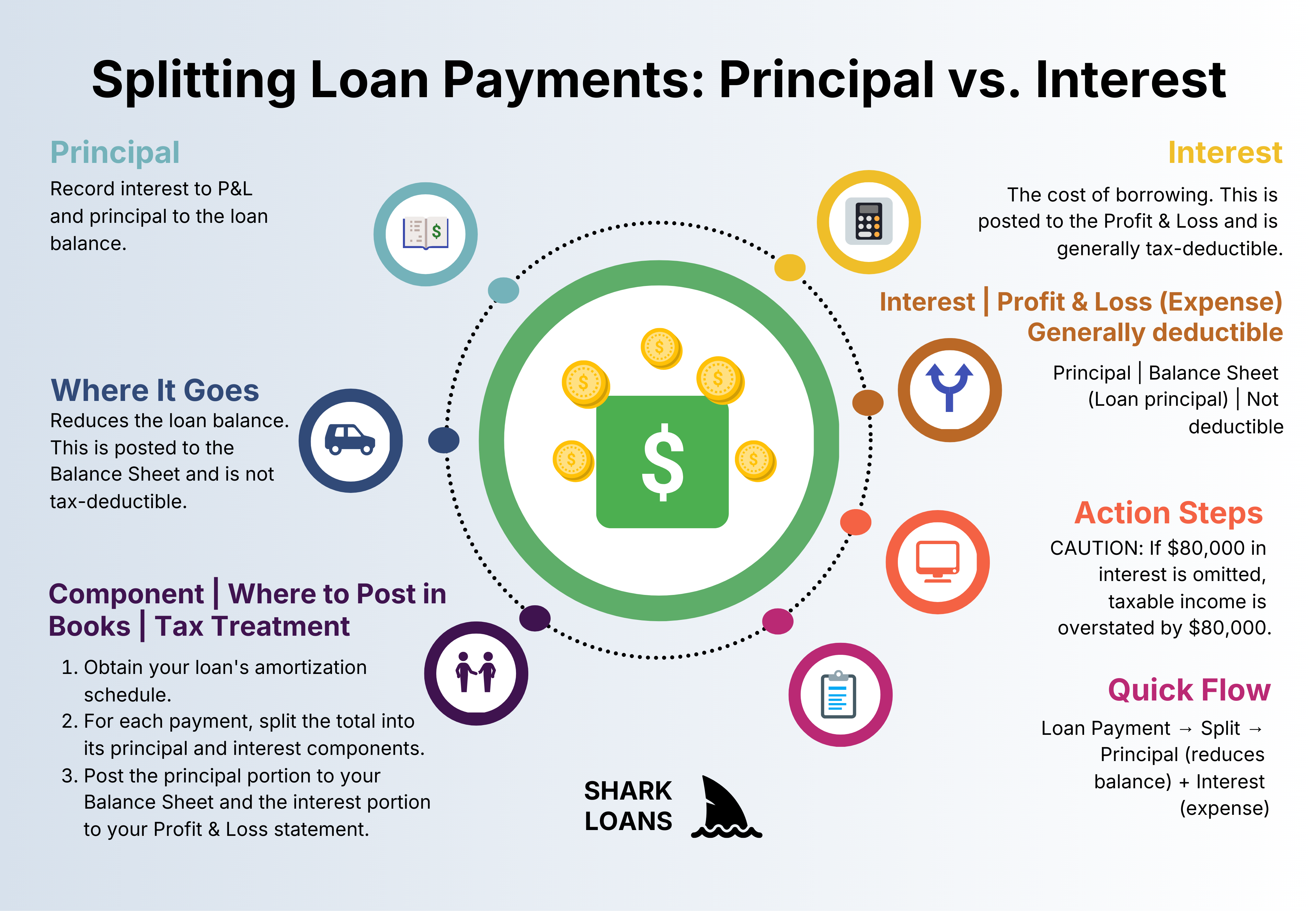

Mistake #1: Poor Recordkeeping (The Costliest Error)

Poor or incomplete books are the root cause of most tax problems. When transactions aren’t categorized correctly, you miss legitimate deductions, inflate profit, and trigger notices. One of the most common errors: mishandling loans.

Loan interest vs. principal (why it matters)

Payments on a business loan include principal (not deductible) and interest (generally deductible). We frequently see the entire payment posted against the loan balance, with no interest recorded as an expense. If you paid $80,000 of interest that never hit your profit and loss, your taxable income is overstated by the same amount. That’s real cash left on the table.

Action steps:

- Use an amortization schedule to split every loan payment between principal and interest.

- Post interest to your profit and loss; reduce only the principal on your balance sheet loan account.

- Reconcile loan statements monthly so year-end adjustments aren’t a scramble.

What good books look like (monthly checklist)

- Bank, credit card, and loan accounts reconciled to statements.

- Clear chart of accounts aligned to tax categories (not a default catch-all).

- Clean accounts payable/receivable; no stale items over 60 days without a reason.

- Capital vs. expense purchases correctly classified.

- Timely financials: a profit and loss and balance sheet by the 10th business day.

Tip: If your CPA only receives bank statements at tax time, they must rebuild a year of accounting. That raises fees, risk, and delays—often with weaker results than doing it continuously.

Mistake #2: Overlooking Eligible Deductions

Missed deductions usually stem from gaps in documentation. Common areas:

- Interest expense: Deduct interest on business loans and credit lines when properly tracked.

- Vehicle use: Either track actual expenses or keep a contemporaneous mileage log. Choose the method that yields the higher deduction.

- Home office: If you use a dedicated space regularly and exclusively for business, you may claim the home office deduction (standard or actual method).

- Professional fees and software: Include CPA, legal, payroll, bookkeeping, and business software subscriptions.

- Contractor payments: Ensure accurate 1099-NEC reporting and capture related costs.

Documentation that defends deductions:

- Receipts or invoices plus proof of payment for material expenses.

- Mileage logs that show date, destination, purpose, and miles.

- Bank/credit statements that match your books.

- Photos or diagrams for a home office, plus square footage and utility records if using actual method.

Mistake #3: Ignoring Estimated Tax Payments

If you owed tax last year and expect to owe this year, you likely need to make quarterly estimated payments. Missing or underpaying estimates leads to penalties and interest.

Safe harbor basics

- Pay at least 90% of your current-year total tax, or

- Pay 100% of last year’s total tax (110% if your prior-year adjusted gross income exceeded $150,000 for most filers).

Quarterly estimates are typically due on April 15, June 15, September 15, and January 15 of the following year. Use 1040-ES vouchers if paying by mail, or pay electronically.

Q1 (Jan–Mar)

- Due date

- April 15

- Notes

- Use safe harbor to avoid penalties

Q2 (Apr–May)

- Due date

- June 15

- Notes

- Date may shift to next business day

Q3 (Jun–Aug)

- Due date

- September 15

- Notes

- Date may shift to next business day

Q4 (Sep–Dec)

- Due date

- January 15 (following year)

- Notes

- Skip if filing and paying in full by Jan 31

| Quarter | Typical Due Date | Notes |

|---|---|---|

| Q1 (Jan–Mar) | April 15 | Use safe harbor to avoid penalties |

| Q2 (Apr–May) | June 15 | Date may shift to next business day |

| Q3 (Jun–Aug) | September 15 | Date may shift to next business day |

| Q4 (Sep–Dec) | January 15 (following year) | Skip if filing and paying in full by Jan 31 |

IRS Audit Red Flags You Can Control

Mismatched 1099/W-2 income

Underreported income is often caught by automated IRS matching programs. If a payer files a 1099-NEC and it’s missing from your return, expect a notice. Before filing, pull your Wage and Income Transcript to confirm what the IRS received.

Excessive or poorly supported deductions

You can deduct ordinary and necessary business expenses, but you must be able to substantiate them. Without receipts, logs, or a clear business purpose, deductions are vulnerable. Home office and vehicle deductions are common and defensible—when documented properly.

Filing Deadlines You Must Track

Calendar-year businesses should note these standard due dates (extensions are for filing, not for paying taxes):

| Return | Form | Standard Due Date | Extended Due Date |

|---|---|---|---|

| Partnership | 1065 | March 15 | September 15 |

| S Corporation | 1120-S | March 15 | September 15 |

| C Corporation | 1120 | April 15 | October 15 |

| Individual | 1040 | April 15 | October 15 |

Always verify the exact dates each year; weekends and holidays can shift the deadlines to the next business day.

A Practical Compliance Workflow for 2025

Monthly

- Import and categorize all transactions; reconcile bank, credit card, and loan accounts.

- Record loan interest vs. principal using amortization schedules.

- Capture mileage and expense receipts (photo and store in your system).

- Generate a profit and loss and balance sheet; review variances vs. prior month.

Quarterly

- Review year-to-date profit and tax projections; adjust estimated payments as needed.

- Close open A/R and A/P; write off uncollectible items with proper approval.

- Review contractor payments and collect W-9s; prepare for 1099s early.

Annually

- Pull your IRS Wage and Income Transcript to confirm 1099s/W-2s on file.

- Complete fixed asset schedules; reconcile inventory if applicable.

- Meet your CPA to finalize tax planning items before year-end, not after.

For fast-growing firms (often $5M+ revenue), consider a more robust accounting platform with stronger controls. The key is less about brand and more about disciplined processes, reconciliations, and documentation.

How to Tell If Your Books Are Working

- Financials delivered by the 10th business day monthly.

- Unreconciled bank/credit transactions under 1% of volume.

- All loans reconciled; interest recorded monthly.

- No more than five uncategorized transactions at month-end.

- Quarterly tax estimates paid on time with supporting calculations.

Bottom Line

If you fix recordkeeping, most other tax problems shrink or disappear. Build a simple monthly close, document deductions as you go, make timely estimates, and verify reported income before you file. That’s how you keep more of your profit and stay audit-ready.

What’s your biggest tax headache for 2025—books, estimates, or audits? Share it below and we’ll point you to a practical next step.

FAQ

Do I need a receipt for every deduction?

For material expenses, yes—keep receipts or invoices plus proof of payment. For small-dollar items, consistent bank/credit records may suffice, but the more documentation you retain, the stronger your audit defense. Certain deductions (like mileage and home office) have specific recordkeeping rules—follow them closely.

What’s the simplest way to track vehicle mileage?

Use a mileage app or a written log and record each trip’s date, destination, purpose, and miles. Keep odometer readings at the start and end of the year. You can choose the standard mileage rate or actual expense method—calculate both and use the larger deduction.

I forgot to include a 1099. What should I do?

Pull your IRS Wage and Income Transcript to confirm what was reported to the IRS. If a 1099 was missed, file an amended return as soon as possible to limit penalties and interest. Going forward, compare your transcripts to your books before you file.

Can I claim a home office if I also work from a coworking space?

Yes, if you have a part of your home used regularly and exclusively for business, you may qualify even if you sometimes work elsewhere. Document the space, square footage, and method used (simplified or actual). Keep utility and housing records if using the actual method.

Do extensions remove penalties for late tax payments?

No. An extension gives you more time to file, not more time to pay. To avoid penalties and interest, pay your expected tax by the original due date. Use quarterly estimates to stay current during the year.

How do I avoid estimated tax penalties?

Use the safe harbor: pay at least 90% of current-year tax or 100% of last year’s tax (110% if your prior-year AGI was over $150,000 for most filers). Revisit your projections quarterly and adjust payments when profits change.

References

Next step

Have a question about your specific situation? Comment with your top 2025 tax concern—recordkeeping, deductions, estimates, or audits—and we’ll share a practical next step you can take this week.